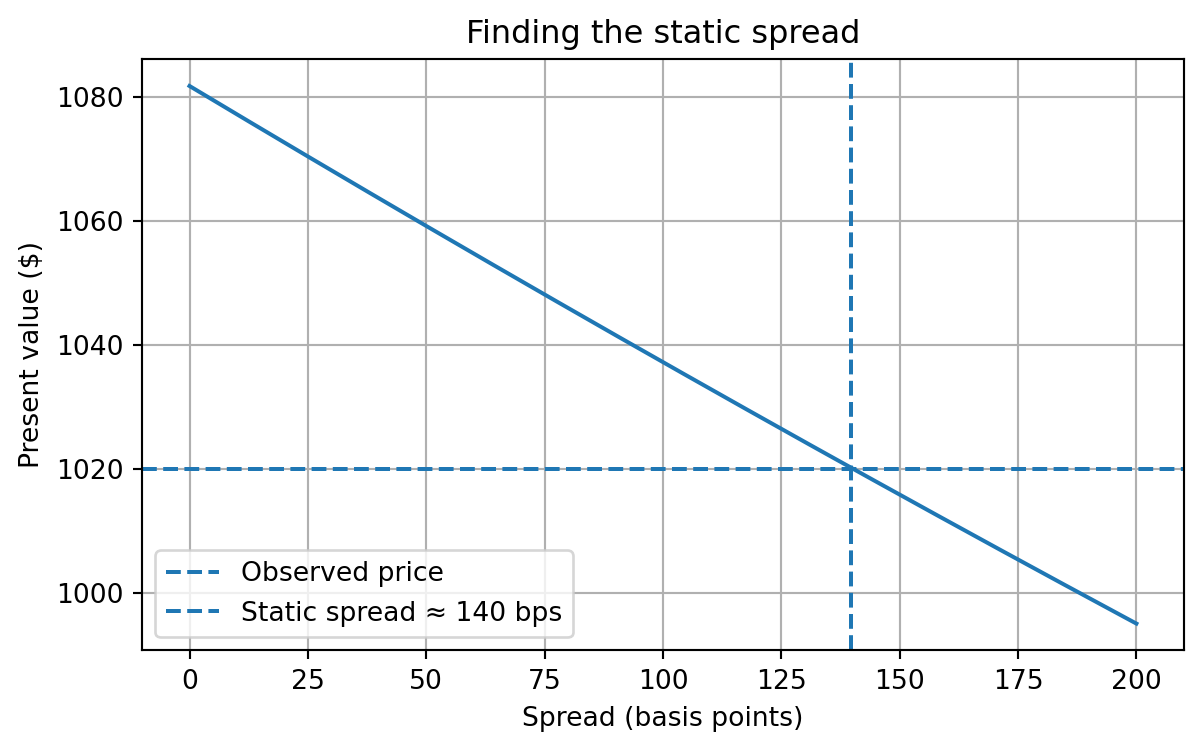

Estimated static spread: 139.8 basis pointsAfter completing this lecture you should be able to:

Historically, fixed-income analysts compared the yield to maturity (YTM) of a corporate bond with the yield of a Treasury security of similar maturity to measure compensation for credit and liquidity risk. The yield spread was defined as

\[ \text{Yield spread} = y_{\text{corporate}} - y_{\text{Treasury}} \]

While straightforward, this measure suffers from several drawbacks:

Single-period perspective. Yield to maturity assumes the investor holds the bond to maturity and reinvests coupons at the YTM. It does not capture the term structure of discount rates or the timing of cash flows.

Ignores embedded options. Callable or putable bonds contain options that significantly affect cash flow timing and risk. Comparing YTMs of a callable corporate bond and a non-callable Treasury ignores the call option’s value. The resulting yield spread blends credit, liquidity, and option premiums, making interpretation difficult.

Assumes parallel shifts. Yield spread analysis implicitly treats interest-rate movements too simply. In reality, yield curves twist, steepen, flatten, and move non-parallel across maturities.

Fails to separate risk components. Credit risk, liquidity risk, and option risk vary across issuers and over time. A simple yield spread bundles them together.

Because of these limitations, modern valuation methods use term-structure models and option-adjusted measures to isolate risks and provide more consistent valuations.

The static spread (also called the I-spread) measures the constant margin over the Treasury spot curve that discounts a bond’s cash flows to its market price. For a bond with cash flows ({CF_{t_i}}) at times (t_1,t_2,,t_n) and Treasury zero rates ({r_{t_i}}), the static spread (s) solves

\[ P = \sum_{i=1}^{n} \frac{CF_{t_i}}{(1 + r_{t_i} + s)^{t_i}} \]

where (P) is the observed price.

Because the same spread (s) is added to all discount rates, the method accounts for the shape of the term structure while producing a single summary measure of compensation for non-Treasury risks. Unlike the yield spread, the static spread discounts each cash flow at a maturity-appropriate rate. That makes it more economically meaningful for coupon bonds, amortizing bonds, and bonds whose cash flows are distributed over time.

However, the static spread still has an important weakness: it discounts promised cash flows, not expected option-adjusted cash flows. For a callable bond, the promised maturity cash flow may never be received if the issuer refinances and calls the bond when rates fall.

Suppose a five-year corporate bond has semiannual coupons of 6 percent, so it pays $30 every six months on a $1,000 face value. The Treasury spot curve for maturities 0.5 years to 5 years is:

\[ \{2.0\%,\, 2.2\%,\, 2.6\%,\, 3.0\%,\, 3.4\%,\, 3.8\%,\, 4.0\%,\, 4.1\%,\, 4.2\%,\, 4.3\%\} \]

Assume the bond trades at $1,020. We estimate the static spread numerically by solving for (s) such that discounted cash flows equal the market price.

Estimated static spread: 139.8 basis pointsIn this example the static spread is about 86 basis points. Economically, that means investors require roughly 86 basis points over the Treasury spot curve to hold this bond.

A callable bond gives the issuer the right, but not the obligation, to redeem the bond before maturity at a specified call price according to a call schedule. The issuer will typically call the bond when prevailing rates fall below the coupon rate, allowing refinancing at a lower borrowing cost.

This embedded call option changes the bond’s economic behavior.

Because the issuer owns the right to call, the investor is effectively short a call option. The callable bond therefore must be worth less than an otherwise identical option-free bond:

\[ V_{\text{callable}} = V_{\text{option-free}} - V_{\text{call option}} \]

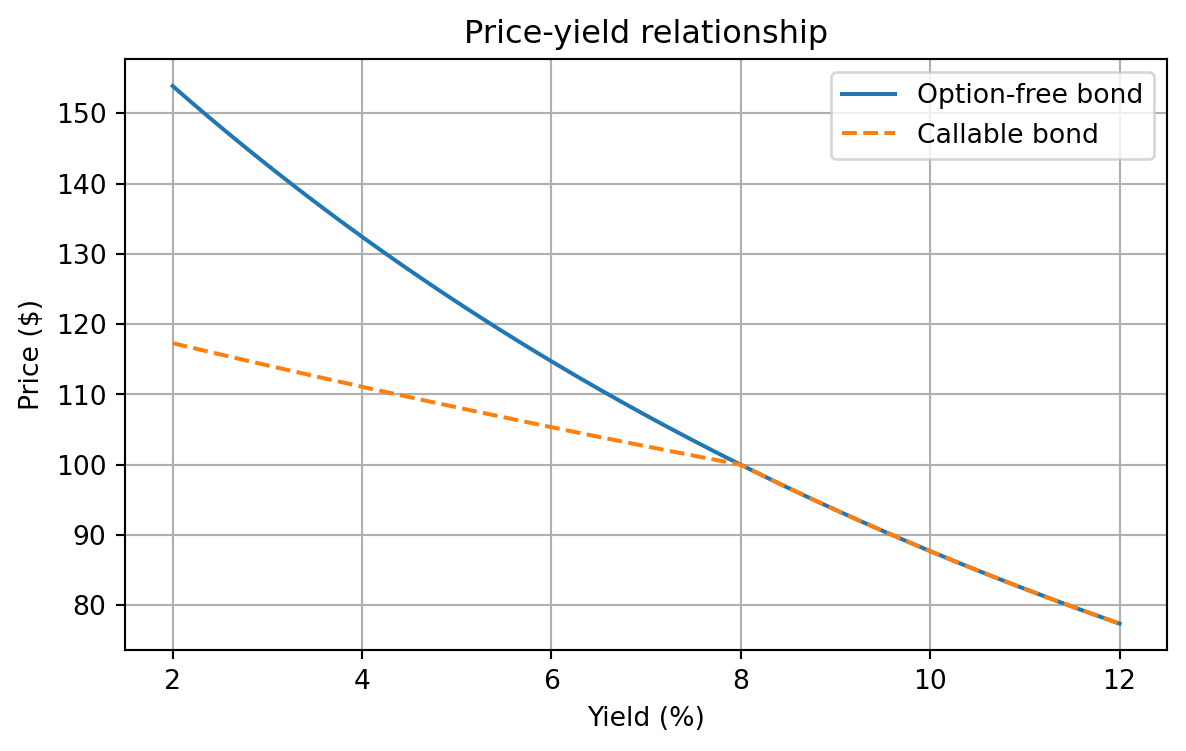

As yields decline, the price of an option-free bond rises at an increasing rate. A callable bond does not. Once rates fall enough, the chance of being called rises sharply, which caps further price appreciation. This gives callable bonds negative convexity over some yield ranges.

Because a callable bond may be redeemed at one of several call dates, investors often compute:

Yield to worst is a practical convention, but it is not a full valuation framework. It does not explicitly model volatility or the contingent nature of cash flows.

To visualize negative convexity, we can compare the price-yield curve of an option-free bond with that of a callable bond.

The callable bond’s price is capped when yields fall enough for calling to become attractive to the issuer. This is the key intuition behind negative convexity.

A bond with an embedded option can be decomposed conceptually into two parts:

For a callable bond:

\[ V_{\text{callable}} = V_{\text{straight}} - V_{\text{call option}} \]

For a putable bond:

\[ V_{\text{putable}} = V_{\text{straight}} + V_{\text{put option}} \]

This decomposition is useful because it tells us exactly where the pricing distortion comes from. The bond itself generates fixed-income cash flows. The option changes the timing and certainty of those cash flows.

The modern approach to valuing bonds with embedded options uses an interest-rate lattice and risk-neutral valuation.

The general logic is:

Build a tree of future short rates.

Determine future bond values at the terminal nodes.

Move backward through the tree using risk-neutral expectations.

At each node, apply the embedded option rule:

The value at time 0 is the bond’s model price.

For an option-free bond, backward induction uses

\[ V_{i,j} = \frac{p\, V_{i+1,j+1} + (1-p)\, V_{i+1,j}}{1 + r_{i,j}} + CF_i \]

where:

For a callable bond:

\[ V_{i,j}^{\text{callable}} = \min\left\{ \frac{p\, V_{i+1,j+1} + (1-p)\, V_{i+1,j}}{1 + r_{i,j}} + CF_i,\ \text{Call Price} \right\} \]

For a putable bond:

\[ V_{i,j}^{\text{putable}} = \max\left\{ \frac{p\, V_{i+1,j+1} + (1-p)\, V_{i+1,j}}{1 + r_{i,j}} + CF_i,\ \text{Put Price} \right\} \]

The lattice is not just a computational trick. It is economically important.

At each date, interest rates may move up or down. That means the bond’s future value is not fixed today. The option’s value comes from this uncertainty.

The lattice lets us model three things at the same time:

This is why spread measures based only on yield to maturity are inadequate for callable and putable bonds.

A useful way to think about the tree is this:

the horizontal direction represents time

the vertical direction represents interest-rate states

each node represents a possible short rate that could prevail at that future date

at each node, someone makes an economic decision:

So the embedded option makes the bond path-dependent. The value depends not only on maturity and coupon, but also on what happens to rates along the way.

To illustrate, consider a three-year bond with annual coupons of 8 on a face value of 100. Assume annual time steps. We first construct a simple short-rate tree directly for intuition.

Suppose the short-rate lattice is:

| Time | State 0 | State 1 | State 2 | State 3 |

|---|---|---|---|---|

| 0 | 5% | |||

| 1 | 4% | 6% | ||

| 2 | 3% | 5% | 7% | |

| 3 | 2% | 4% | 6% | 8% |

Assume:

This simplified tree is excellent for teaching because it isolates the core logic of backward induction.

We now price the bond by hand using backward induction.

At year 3 the bond pays final coupon plus principal:

\[ 108 = 100 + 8 \]

So the year-3 node values are:

| Node at Year 3 | Bond Value |

|---|---|

| 2% state | 108.00 |

| 4% state | 108.00 |

| 6% state | 108.00 |

| 8% state | 108.00 |

At each year-2 node, the option-free bond value is:

\[ V = \frac{0.5 \times 108 + 0.5 \times 108}{1 + r} + 8 = \frac{108}{1+r} + 8 \]

\[ V = \frac{108}{1.03} + 8 = 104.8544 + 8 = 112.8544 \]

\[ V = \frac{108}{1.05} + 8 = 102.8571 + 8 = 110.8571 \]

\[ V = \frac{108}{1.07} + 8 = 100.9346 + 8 = 108.9346 \]

So the option-free values at year 2 are:

| Node at Year 2 | Hold Value |

|---|---|

| 3% state | 112.85 |

| 5% state | 110.86 |

| 7% state | 108.93 |

Because the bond is callable at par from year 2 onward, the issuer will compare the hold value with the call price of 100.

For the callable bond:

\[ V^{\text{callable}} = \min\{\text{Hold Value},\ 100\} \]

Thus:

| Node at Year 2 | Hold Value | Callable Value |

|---|---|---|

| 3% state | 112.85 | 100.00 |

| 5% state | 110.86 | 100.00 |

| 7% state | 108.93 | 100.00 |

This is the key economic point: at year 2 the straight bond is worth more than 100 in every state, so the issuer calls the bond immediately in every state.

Now compute the option-free bond values at year 1 using the option-free year-2 values.

\[ V = \frac{0.5(110.8571) + 0.5(112.8544)}{1.04} + 8 \]

\[ V = \frac{111.8558}{1.04} + 8 = 107.5537 + 8 = 115.5537 \]

\[ V = \frac{0.5(108.9346) + 0.5(110.8571)}{1.06} + 8 \]

\[ V = \frac{109.8959}{1.06} + 8 = 103.6754 + 8 = 111.6754 \]

So:

| Node at Year 1 | Option-Free Value |

|---|---|

| 4% state | 115.55 |

| 6% state | 111.68 |

Now do the same using the callable values at year 2, which are both 100 in every reachable state.

\[ V = \frac{0.5(100) + 0.5(100)}{1.04} + 8 = \frac{100}{1.04} + 8 = 96.1538 + 8 = 104.1538 \]

\[ V = \frac{100}{1.06} + 8 = 94.3396 + 8 = 102.3396 \]

So:

| Node at Year 1 | Callable Value |

|---|---|

| 4% state | 104.15 |

| 6% state | 102.34 |

\[ V_0^{\text{straight}} = \frac{0.5(115.5537) + 0.5(111.6754)}{1.05} + 8 \]

\[ V_0^{\text{straight}} = \frac{113.6146}{1.05} + 8 = 108.2044 + 8 = 116.2044 \]

\[ V_0^{\text{callable}} = \frac{0.5(104.1538) + 0.5(102.3396)}{1.05} + 8 \]

\[ V_0^{\text{callable}} = \frac{103.2467}{1.05} + 8 = 98.3302 + 8 = 106.3302 \]

The call option value is the difference between the straight bond value and the callable bond value:

\[ V_{\text{call option}} = V_{\text{straight}} - V_{\text{callable}} \]

\[ V_{\text{call option}} = 116.2044 - 106.3302 = 9.8742 \]

So in this example:

| Quantity | Value |

|---|---|

| Option-free bond price | 116.20 |

| Callable bond price | 106.33 |

| Embedded call option value | 9.87 |

This example teaches three important things.

First, the callable bond is worth less than the straight bond because the issuer owns the call option.

Second, the option matters most when rates are low and the straight bond is worth substantially above par. In those states, the issuer will refinance and cap the investor’s upside.

Third, the lattice makes the exercise decision explicit at each node. That is the real advantage of the model.

The following code reproduces the lattice valuation for the option-free and callable bond.

Option-free price: 116.2043

Callable price: 106.3302

Call option value: 9.8740In more formal models, rates evolve according to a short-rate process rather than being assigned directly. For example, with a lognormal up and down structure:

\[ u = e^{\sigma \sqrt{\Delta t}}, \qquad d = \frac{1}{u} \]

and a stylized risk-neutral probability

\[ p = \frac{e^{r \Delta t} - d}{u - d} \]

A short-rate tree can then be generated from an initial rate (r_0). The point of such a tree is not just to create possible future rates, but to calibrate those rates so that the model reproduces today’s observed yield curve.

Time 0: [np.float64(0.05)]

Time 1: [np.float64(0.0452), np.float64(0.0553)]

Time 2: [np.float64(0.0409), np.float64(0.05), np.float64(0.0611)]

Time 3: [np.float64(0.037), np.float64(0.0452), np.float64(0.0553), np.float64(0.0675)]

Risk-neutral probability: 0.7309In practice, professional valuation systems use calibrated models such as Ho-Lee, Black-Derman-Toy, Hull-White, or Black-Karasinski. The teaching objective here is not the full calibration machinery, but the economic structure of the valuation.

The lattice framework can be extended to corporate bonds in several ways.

One approach is to add a credit spread (s) to each node’s short rate:

\[ r_{i,j}^{\text{risky}} = r_{i,j} + s \]

Another is to introduce default probabilities and recovery assumptions directly into the tree. Then the node value reflects both survival and default scenarios.

These extensions are important in practice because many callable bonds are corporate or structured products whose spreads reflect both credit and optionality.

Real-world implementation is harder than the classroom example suggests. A practical model must decide:

Even so, the lattice remains one of the clearest frameworks for understanding the economics of embedded options.

The option-adjusted spread measures the constant spread over the risk-free curve that equates the model price of a bond, after adjusting for embedded option effects, to its market price.

Unlike the static spread, the OAS discounts expected path-dependent cash flows, not simply promised contractual cash flows.

A general expression is:

\[ P_{\text{market}} = \sum_{\text{paths}} \frac{\Pr(\text{path}) \times CF_{\text{path}}} {\prod_{i}(1 + r_{i,\text{path}} + s_{\text{OAS}})^{\Delta t}} \]

where the sum runs over all interest-rate paths.

Suppose two bonds have the same nominal spread over Treasuries, but one is callable and the other is not. The callable bond’s spread partly compensates the investor for being short the call option. The OAS attempts to strip out that option effect.

That makes OAS a cleaner measure of relative value when embedded options matter.

So for bonds with embedded options, OAS is usually the economically relevant spread measure.

If a callable bond has a nominal spread of 150 basis points but an OAS of 100 basis points, then roughly 50 basis points of the nominal spread reflect the call option rather than pure credit or liquidity compensation.

For bonds with embedded options, traditional Macaulay duration and convexity are inadequate because cash flows depend on the future path of interest rates.

Instead, we use effective duration and effective convexity, which are based on revaluing the bond after small changes in the entire yield curve.

Let:

Then:

\[ D_e = \frac{P_- - P_+}{2 P_0 \Delta y} \]

\[ C_e = \frac{P_- + P_+ - 2P_0}{P_0 (\Delta y)^2} \]

For callable bonds, effective duration is often shorter than for an otherwise similar option-free bond, and effective convexity may become small or even negative when the bond is likely to be called.

Using the callable bond in our lattice example, we can shift the entire short-rate tree up and down by 50 basis points and reprice the bond.

Base price: 106.3302

Price with rates up: 105.4363

Price with rates down: 107.2369

Effective duration: 1.6934

Effective convexity: 4.7739Because the call feature limits upside when rates fall, the callable bond’s price response is asymmetric. That is exactly what effective convexity is designed to capture.