Lecture 2: Bond Pricing and Yield Measures

Learning Objectives

By the end of this lecture you should be able to:

- Explain the time value of money and calculate future values and present values for cash‑flows.

- Compute the price of a bond by discounting expected cash‑flows at an appropriate discount rate.

- Describe how bond prices move in response to changes in yield and why the price–yield relationship is convex.

- Relate coupon rate and yield to a bond’s trading status (par, premium or discount) and recognise how prices evolve as a bond approaches maturity (pull to par).

- Identify factors—market interest rates, credit risk, liquidity, economic expectations, tax policy and inflation—that cause bond prices to change.

- Describe complications in bond pricing arising from embedded options, floating‑rate structures and inverse floaters.

- Explain how bonds are quoted clean and dirty, and compute accrued interest.

- Compute yields using the present‑value relationship: current yield, yield to maturity, yield to call, yield to put, yield to sinker and yield to worst, as well as the yield for a portfolio and the cash‑flow yield for amortising securities.

- Compute the discount margin for a floating‑rate security and explain why this margin differs from conventional yield measures.

- Identify the sources of a bond’s total return—coupon interest, reinvestment income and capital gain or loss—and discuss reinvestment risk.

- Use total return and horizon analysis to evaluate the realised performance of a bond or bond strategy under explicit assumptions about reinvestment rates and future yields.

- Measure changes in yield using absolute (basis‑point) and relative (percentage) conventions.

1 The Time Value of Money

A fundamental principle underlying all fixed income valuation is the time value of money. A dollar received today is worth more than a dollar received in the future because the dollar today can be invested to earn interest. When an investor purchases a bond, the investor is exchanging money today for a stream of future cash flows. To determine whether this exchange is fair, we must be able to compare money received at different points in time. The tool that allows us to do this is present value and future value analysis.

In fixed income markets, virtually every valuation problem can be reduced to one question:

What is the present value of a set of future cash flows?

To answer this question, we must first understand how money grows over time and how future cash flows are discounted back to the present.

1.1 Future Value

Suppose an investor invests an amount \(P_0\) today at an interest rate \(r\) per period. After one period, the investment grows to

\[ P_1 = P_0(1+r). \]

After two periods, the investment grows to

\[ P_2 = P_0(1+r)^2. \]

After \(n\) periods, the investment grows to

\[ P_n = P_0(1+r)^n. \]

This is the future value of the investment. The key idea behind this formula is compound interest: interest earned each period is reinvested and itself earns interest in future periods. In fixed income markets, compounding plays a central role because coupon payments are often reinvested, and the return on a bond depends not only on coupon payments but also on the interest earned on reinvested coupons.

NoteWorked Example

Future Value

Suppose a pension fund invests $10,000,000 at a stated annual interest rate of 9.2% for 6 years.

Annual compounding. Interest is credited once per year, so the investment earns 9.2% each year for six years:

\[ P_6 = 10{,}000{,}000(1.092)^6 \approx 16{,}956{,}500. \]

The balance is approximately $16.96 million after six years.

Semi-annual compounding. Interest is credited every six months at half the annual rate, so there are \(2 \times 6 = 12\) compounding periods and the six-month rate is \(0.092/2 = 0.046\):

\[ P_6 = 10{,}000{,}000\left(1 + \frac{0.092}{2}\right)^{12} = 10{,}000{,}000(1.046)^{12} \approx 17{,}154{,}585. \]

Equivalently, \(P_T = P_0\left(1 + \frac{r}{m}\right)^{mT}\) with \(r = 0.092\), \(T = 6\), and \(m = 2\) compounding intervals per year. More frequent compounding yields a higher terminal value (here about $17.15 million) because interest is reinvested sooner within each year.

1.2 Future Value of an Ordinary Annuity

An ordinary annuity is a series of equal payments made at the end of each period. Coupon payments on most bonds are an example of an ordinary annuity.

Suppose a payment \(C\) is made at the end of each period for \(n\) periods, and the interest rate is \(r\). The future value of these payments at time \(n\) is

\[ FV = C \left( \frac{(1+r)^n - 1}{r} \right). \]

NoteDerivation: Future Value of an Ordinary Annuity

Suppose a payment \(C\) is made at the end of each period for \(n\) periods, and the interest rate per period is \(r\).

The cash flows can be represented as:

\[ \begin{aligned} \text{Time 1:} & \quad C \\ \text{Time 2:} & \quad C \\ & \vdots \\ \text{Time n:} & \quad C \end{aligned} \]

Each payment earns interest from the time it is made until the end of the period \(n\):

- The first payment (at time 1) is invested for \(n-1\) periods: \(C(1+r)^{n-1}\)

- The second payment is invested for \(n-2\) periods: \(C(1+r)^{n-2}\)

- …

- The last payment (at time \(n\)) is made at the end and earns no additional interest: \(C(1+r)^0 = C\)

The future value at time \(n\) is the sum:

\[ FV = C(1+r)^{n-1} + C(1+r)^{n-2} + \cdots + C(1+r)^0 \]

Factoring out \(C\):

\[ FV = C \left[ (1+r)^{n-1} + (1+r)^{n-2} + \dots + 1 \right] \]

This is a geometric series with \(n\) terms, ratio \((1+r)\):

\[ FV = C \cdot \frac{(1+r)^n - 1}{r} \]

This is the future value formula for an ordinary annuity.

This formula shows that the future value of an annuity depends on both the number of payments and the interest rate at which the payments are reinvested. This is important in fixed income because the total return from a bond depends heavily on the reinvestment of coupon payments.

NoteReinvestment of Coupon Payments: 15-Year Bond Example

Setup

A portfolio manager purchases $20 million par value of a 15-year bond with a 10% annual coupon, paid once per year.

- Annual coupon payment: \(0.10 \times 20{,}000{,}000 = 2{,}000{,}000\)

- Coupons are reinvested at 8% annually

- Horizon: 15 years

Step 1 — Future value of reinvested coupons

The coupon stream is an ordinary annuity of $2,000,000 per year. Its future value is:

\[ FV = A \cdot \frac{(1+r)^n - 1}{r} \]

\[ FV = 2{,}000{,}000 \cdot \frac{(1.08)^{15} - 1}{0.08} = 2{,}000{,}000 \cdot 27.152125 = 54{,}304{,}250 \]

Step 2 — Decomposition of coupon value

- Total coupon cash received: \(15 \times 2{,}000{,}000 = 30{,}000{,}000\)

- Interest earned from reinvestment: \(54{,}304{,}250 - 30{,}000{,}000 = 24{,}304{,}250\)

Step 3 — Total wealth at maturity

- Par (maturity) value: \(20{,}000{,}000\)

- Future value of reinvested coupons: \(54{,}304{,}250\)

\[ \text{Total future value} = 20{,}000{,}000 + 54{,}304{,}250 = 74{,}304{,}250 \]

Final Breakdown

| Component | Amount (USD) |

|---|---|

| Par value at maturity | 20,000,000 |

| Coupon payments (sum) | 30,000,000 |

| Interest from reinvesting coupons | 24,304,250 |

| Total future value (after 15 years) | 74,304,250 |

Key point

A substantial portion of terminal wealth comes from reinvestment income, not just coupons or principal. This is the essence of reinvestment risk.

1.3 Present Value

Present value is the reverse of future value. Instead of asking how much an investment today will grow to in the future, we ask:

How much is a future cash flow worth today?

If a payment of \(F\) will be received in \(n\) periods and the interest rate is \(r\), the present value is

\[ PV = \frac{F}{(1+r)^n}. \]

This formula is called discounting, and the interest rate \(r\) is called the discount rate. In fixed income markets, the discount rate reflects the required yield on a bond, which depends on interest rates, credit risk, liquidity, and other factors.

NoteWorked Example

Present Value

Suppose an investor will receive $1,000 in 3 years and the discount rate is 5%.

\[ PV = \frac{1000}{(1.05)^3} = 863.84. \]

The present value of $1,000 received in three years is $863.84.

1.4 Present Value of a Series of Future Cash Flows

Most bonds pay multiple cash flows: periodic coupon payments and the principal at maturity. The present value of a series of future cash flows is simply the sum of the present values of each individual cash flow.

If the cash flows are \(CF_1, CF_2, \dots, CF_n\), then

\[ PV = \sum_{t=1}^{n} \frac{CF_t}{(1+r)^t}. \]

This is the fundamental bond pricing formula. Every bond pricing problem is an application of this equation.

NoteWorked Example

Present Value of Multiple Cash Flows

Suppose a bond pays $60 in one year, $60 in two years, and $1,060 in three years. If the discount rate is 5%:

\[ PV = \frac{60}{1.05} + \frac{60}{1.05^2} + \frac{1060}{1.05^3} = 1026.71. \]

This is the price of the bond.

1.5 Present Value of an Ordinary Annuity

If a bond pays a fixed coupon \(C\) each period for \(n\) periods, the present value of the coupon payments is the present value of an ordinary annuity:

\[ PV = C \left( \frac{1 - (1+r)^{-n}}{r} \right). \]

The price of a bond can therefore be written as

\[ P = C \left( \frac{1 - (1+r)^{-n}}{r} \right) + \frac{F}{(1+r)^n}. \]

This formula shows that a bond is simply the present value of an annuity (coupon payments) plus the present value of a single payment (principal).

NoteDerivation: Present Value of an Ordinary Annuity

To derive the present value formula for an ordinary annuity (a series of \(n\) payments of \(C\) each, received at the end of each period, discounted at rate \(r\)):

The present value is the sum of the present values of all payments:

\[ PV = \frac{C}{(1 + r)} + \frac{C}{(1 + r)^2} + \cdots + \frac{C}{(1 + r)^n} \]

This is a geometric series:

- First term \(= \frac{C}{1 + r}\)

- Common ratio \(= \frac{1}{1 + r}\)

The sum of a geometric series with \(n\) terms is:

\[ S_n = a \left( \frac{1 - q^n}{1 - q} \right) \]

Plugging in the values:

- \(a = \frac{C}{1 + r}\)

- \(q = \frac{1}{1 + r}\)

So,

\[ PV = \frac{C}{1 + r} \left( \frac{1 - \left( \frac{1}{1 + r} \right)^n}{1 - \frac{1}{1 + r}} \right) \]

Simplify the denominator:

\[ 1 - \frac{1}{1 + r} = \frac{(1 + r) - 1}{1 + r} = \frac{r}{1 + r} \]

Therefore:

\[ PV = \frac{C}{1 + r} \cdot \frac{1 - (1 + r)^{-n}}{r / (1 + r)} = C \left( \frac{1 - (1 + r)^{-n}}{r} \right) \]

This yields the familiar formula for the present value of an ordinary annuity:

\[ PV = C \left( \frac{1 - (1 + r)^{-n}}{r} \right) \]

1.6 Present Value When Payments Occur More Than Once per Year

In many bond markets, coupon payments are made semiannually, meaning twice per year. Some securities pay quarterly or monthly.

When payments occur more than once per year, we must adjust both the interest rate and the number of periods.

If the annual interest rate is \(r\) and there are \(m\) payments per year, then:

- Interest rate per period = \(\frac{r}{m}\)

- Number of periods = \(n \times m\)

The present value formula becomes

\[ PV = \sum_{t=1}^{nm} \frac{CF_t}{\left(1+\frac{r}{m}\right)^t}. \]

NoteWorked Example

Semiannual Bond Pricing

Suppose a bond pays $80 per year in coupons, paid semiannually, for 5 years. The required yield is 6%.

- Semiannual coupon = $40

- Semiannual yield = 3%

- Number of periods = 10

\[ P = 40 \left( \frac{1 - (1.03)^{-10}}{0.03} \right) + \frac{1000}{(1.03)^{10}}. \]

This gives the price of the bond.

1.7 Key Insight

The most important idea in fixed income valuation is:

The price of any fixed income security is the present value of its expected future cash flows discounted at an appropriate discount rate.

2 Pricing a Bond

The price of a bond is equal to the present value of its expected future cash flows. These cash flows consist of periodic coupon payments and the repayment of principal at maturity. Therefore, a bond can be viewed as a financial instrument that converts a series of future payments into a present value.

If a bond has coupon payment \(C\), face value \(F\), maturity \(n\), and required yield \(r\), the price of the bond is

\[ P = \sum_{t=1}^{n} \frac{C}{(1+r)^t} + \frac{F}{(1+r)^n}. \]

This formula shows that bond pricing is simply an application of present value. The required yield used to discount the cash flows reflects market interest rates, credit risk, liquidity, and other factors.

NoteWorked Example

Bond Pricing Example

Suppose a bond has a face value of \(\$1,000\), pays an annual coupon of \(\$50\) \((C=50)\), matures in 3 years, \((n=3)\), and the required yield is \(6\%\), \((r=0.06)\). What is the price of the bond?

First, calculate the present value of each coupon payment and the face value:

\[ \begin{aligned} \text{Price} &= \frac{50}{(1+0.06)^1} + \frac{50}{(1+0.06)^2} + \frac{50}{(1+0.06)^3} + \frac{1000}{(1+0.06)^3} \\ &= \frac{50}{1.06} + \frac{50}{1.1236} + \frac{50}{1.191016} + \frac{1000}{1.191016} \\ &= 47.17 + 44.51 + 42.00 + 839.62 \\ &= \textbf{\$973.30} \end{aligned} \]

So, the bond price is $973.30.

2.1 Pricing Zero-Coupon Bonds

A zero-coupon bond makes only one payment at maturity and does not pay periodic coupons. Therefore, its price is simply the present value of the maturity value.

\[ P = \frac{F}{(1+r)^n}. \]

Zero-coupon bonds are particularly useful for understanding the relationship between interest rates and bond prices because there is only one cash flow.

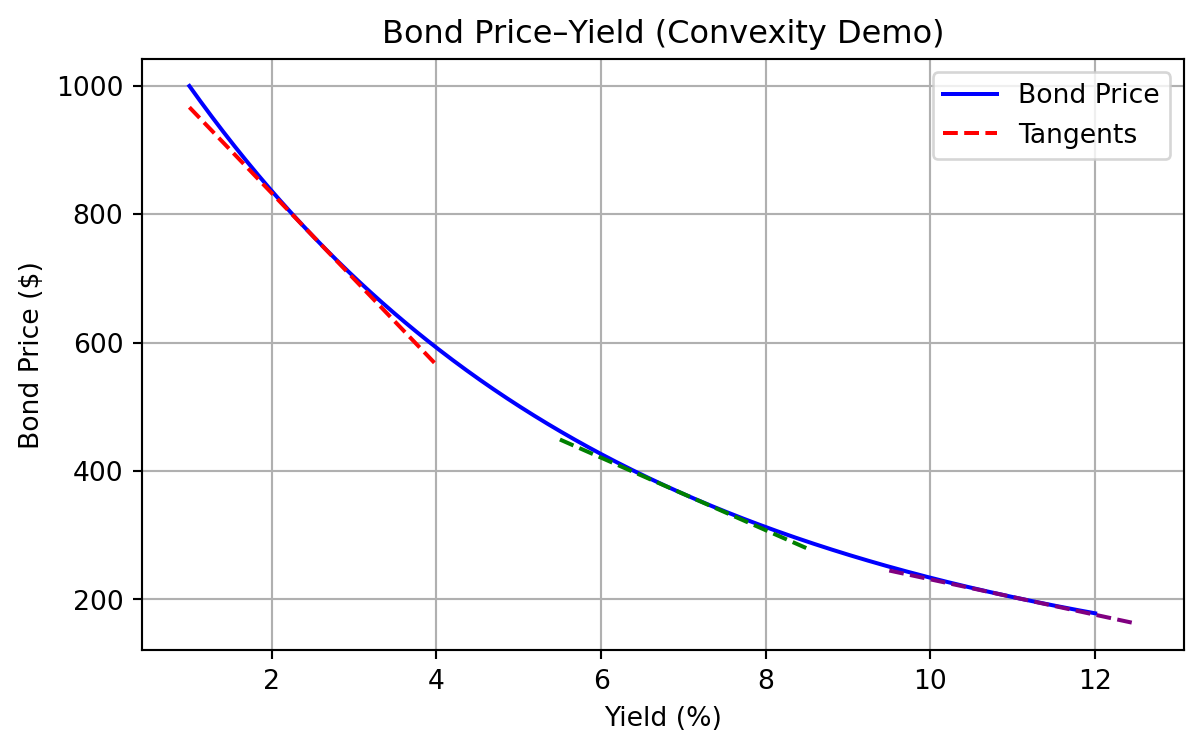

3 Price–Yield Relationship

One of the most important relationships in fixed income markets is the inverse relationship between bond prices and yields. When required yields increase, the present value of future cash flows decreases, and therefore the bond price falls. When required yields decrease, the present value of future cash flows increases, and therefore the bond price rises.

This inverse relationship exists because the bond’s cash flows are fixed while the discount rate changes.

The relationship between bond price and yield is not just inverse and curved—it’s significantly convex. Convexity refers to the “bowed out” shape of the price-yield curve, which becomes even more noticeable for bonds with longer maturities and lower coupons. The greater the convexity, the more rapidly the bond’s price rises as yields fall and the more gently it drops as yields rise. Highly convex bonds are more responsive to changes in yield, offering increasing protection and upside as rates fall.

The graph above demonstrates the inverse and nonlinear (convex) relationship between bond price and yield. As yield increases, bond price falls, and vice versa. Notice the curve bows outward—this is convexity.

4 Relationship Between Coupon Rate, Required Yield, and Price

The relationship between the coupon rate and the required yield determines whether a bond sells at par, at a premium, or at a discount.

| Coupon Rate vs Yield | Bond Price |

|---|---|

| Coupon rate = Yield | Price = Par |

| Coupon rate > Yield | Price > Par (Premium) |

| Coupon rate < Yield | Price < Par (Discount) |

If the coupon rate is higher than the market yield, the bond pays more interest than comparable bonds, so investors are willing to pay more than par. If the coupon rate is lower than the market yield, the bond pays less interest than comparable bonds, so investors will only buy it at a discount.

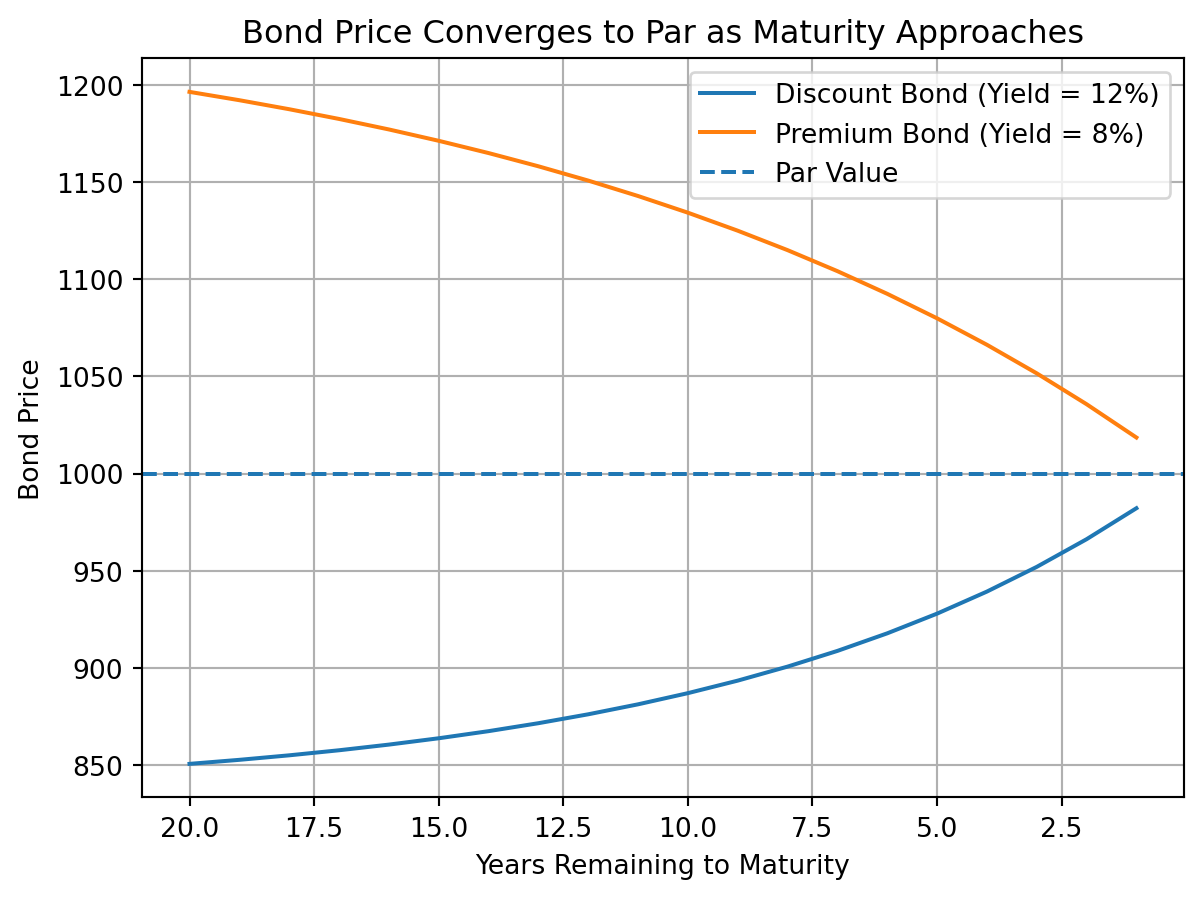

5 Relationship Between Bond Price and Time if Interest Rates Are Unchanged

If interest rates remain unchanged, the price of a bond will move toward its face value as it approaches maturity. This is known as pull to par.

- A premium bond will decline in price over time.

- A discount bond will increase in price over time.

- A bond selling at par will remain at par.

This occurs because the present value of the principal repayment becomes less sensitive to discounting as the bond approaches maturity.

ImportantTime Path of Bond Price as Maturity Approaches

The figure below shows how the price of a 20-year 10% coupon bond moves toward par as it approaches maturity when market yields remain unchanged. A bond selling at a discount rises toward par, while a bond selling at a premium falls toward par.

6 Reasons for the Change in the Price of a Bond

Bond prices change for several reasons. The most important factor is changes in market interest rates, but other factors also affect bond prices:

- Changes in the level of interest rates

- Changes in credit risk of the issuer

- Changes in liquidity of the bond

- Changes in tax treatment

- Changes in inflation expectations

- Changes in economic conditions

Understanding these factors is essential for fixed income portfolio management because bond prices can change even if interest rates remain constant.

7 Complications in Pricing Bonds

In practice, bond pricing is more complicated than the basic present value formula suggests. Several issues arise in real-world bond pricing.

7.1 Next Coupon Payment Due in Less Than Six Months

Bonds often trade between coupon payment dates. When this happens, the buyer must compensate the seller for the interest that has accrued since the last coupon payment. Because the next coupon payment is less than a full period away, the bond must be priced using fractional periods.

Let

\[ v = \frac{\text{days from settlement to next coupon}}{\text{days in coupon period}} \]

Then the price of a bond between coupon dates is

\[ P = \sum_{t=1}^{n} \frac{C}{(1 + r)^{t - 1 + v}} + \frac{M}{(1 + r)^{n - 1 + v}} \]

where:

- \(C\) = coupon payment per period

- \(M\) = maturity (face) value

- \(n\) = number of remaining coupon payments

- \(r\) = yield per period

- \(v\) = fraction of coupon period until next payment

The exponent \(t - 1 + v\) reflects that the next coupon payment occurs in less than one full period, and all remaining cash flows must be discounted accordingly.

This price is called the full price or dirty price of the bond.

The clean price is obtained by subtracting accrued interest:

\[ \text{Clean Price} = \text{Dirty Price} - \text{Accrued Interest} \]

Accrued interest is calculated as

\[ \text{Accrued Interest} = C \times \frac{\text{days since last coupon}}{\text{days in coupon period}}. \]

7.2 Cash Flows May Not Be Known

For some bonds, the future cash flows are uncertain. Examples include:

- Callable bonds

- Putable bonds

- Mortgage-backed securities

- Floating-rate securities

In these cases, cash flows depend on future interest rates or borrower behavior.

7.3 Determining the Appropriate Required Yield

The required yield depends on several factors:

- Risk-free rate

- Credit risk

- Liquidity risk

- Time to maturity

- Tax considerations

Choosing the correct discount rate is often the most difficult part of bond valuation.

7.4 One Discount Rate Applicable to All Cash Flows

The basic bond pricing formula assumes that all cash flows are discounted at the same interest rate. In reality, different cash flows should be discounted using different interest rates based on their maturity. This leads to the concept of the term structure of interest rates, which will be discussed later in the course.

8 Pricing Floating-Rate and Inverse-Floating-Rate Securities

Many bonds do not pay a fixed coupon. Instead, each coupon is tied to a short-term reference rate (for example a Treasury bill rate, SOFR, or—historically—LIBOR) and sometimes to a fixed spread or a formula. The two main structures below are floating-rate notes (floaters) and inverse floaters.

8.1 Floating-rate notes (floaters)

What they are. On each reset date, the issuer sets the coupon for the next period as a reference rate plus a fixed margin (spread), e.g.

\[ \text{coupon rate for the period} = \text{reference rate} + \text{margin}. \]

The bond pays that rate on par for that period; at the next reset, the coupon changes again. Caps and floors may limit how high or low the coupon can go.

Why they exist. Borrowers (corporates, banks, governments) use floaters when they prefer funding costs that move with short rates instead of locking in a long-term fixed coupon. Investors use them when they want income that resets with money-market conditions, limiting sensitivity of price to small parallel shifts in the curve right after a reset.

Who uses them. Cash-rich institutions (money managers, corporate treasuries), bank treasury desks, and liability-driven investors often hold floaters as short-duration credit or liquidity instruments; issuers include banks and non-financial corporates.

How they are priced. Conceptually, price is still the present value of expected future cash flows, but those cash flows depend on future reference rates. Right after a coupon reset, if credit risk is unchanged, a plain floater with no unusual options often trades close to par because the next coupon is already aligned with current short rates. Between resets, the accrued value of the current coupon makes the clean price drift slightly away from par. For yield-style measures, practitioners often use a spread over the reference (e.g. discount margin), which is developed later in this lecture in more detail.

What moves the price. Key factors include: changes in the issuer’s credit spread (the margin the market demands over the reference); time to the next reset; the shape of short-rate expectations; liquidity; and any embedded options (caps, floors, call features). A widening credit spread lowers price even if the reference rate is unchanged.

TipIntuition: Why a floater often hugs par

After a reset, the next coupon is set from today’s short rate. If nothing else changes, discounting that near–market coupon at a comparable short discount rate brings value back toward face value—unlike a fixed-rate bond, whose old coupon can be far above or below the market rate.

NoteExample: Quarterly reset

A floater pays quarterly with a margin of 0.40% (40 bp) over 3-month SOFR. If SOFR is 5.00% on the reset date, the coupon for the next quarter is 5.40% annualised (paid according to the day-count convention in the prospectus). If SOFR jumps to 5.50% at the next reset, the following quarter’s coupon becomes 5.90%. The investor’s cash income rises with short rates without needing to sell the bond.

8.2 Inverse floating-rate bonds

What they are. An inverse floater pays a coupon that falls when the reference rate rises and rises when it falls. A common pattern is

\[ \text{coupon} = K - a \times \text{reference rate}, \]

where \(K\) is a fixed base and \(a > 0\) is a leverage coefficient. There is usually a floor (coupon cannot go below zero or a stated minimum) and sometimes a cap. The structure can be created directly by the issuer or synthetically by combining fixed-rate bonds and floaters (for example in structured mortgage deals).

Why they exist. Issuers and structurers create inverse floaters to match demand from investors who want a bet on falling rates or who seek higher initial income in exchange for taking concentrated rate risk. They also appear as tranches that reallocate interest-rate risk within a larger pool of collateral.

Who uses them. Typically sophisticated institutional investors who understand negative duration and convexity—not a retail “buy and hold” core holding. Portfolio managers may use them tactically or as part of structured products.

How they are priced. Again, price equals the present value of expected future coupons and principal, but each future coupon depends on the path of the reference rate (and on floors/caps). Because coupons move the wrong way for rate levels, effective interest-rate sensitivity is often much larger than for a fixed-rate bond of the same maturity: duration can be long or even negative in some regions, and prices can be very volatile.

What moves the price. Besides credit spread and liquidity (as for any bond), the main drivers are: the level and expected path of the reference rate; volatility of rates (optionality from floors/caps matters); leverage \(a\) in the coupon formula; and time to each reset. A rate rally can lift both the fixed-rate market and inverse-floater coupons, amplifying moves.

TipIntuition: Inverse means amplified rate exposure

A fixed-rate bond loses principal value when yields spike. An inverse floater often also cuts your coupon when rates rise—so you can be hit on both price and income. When rates fall, the opposite can feel like a “double win,” which is why these structures are sometimes marketed for rate-bullish views—and why they require careful risk limits.

NoteExample: Simple inverse coupon

Suppose \(K = 12\%\) and \(a = 1\), with the reference rate equal to 3-month SOFR (annualised). If SOFR is 3%, the coupon is \(12\% - 3\% = 9\%\). If SOFR rises to 7%, the coupon falls to \(12\% - 7\% = 5\%\). If the formula hits a floor of 0%, very high SOFR would clamp the coupon at 0% instead of turning negative.

8.3 Relationship between floaters and inverse floaters: collateral and repackaging

Standalone vs structured. A corporate or sovereign floater is usually a direct promise by the issuer: the coupon formula is chosen for funding or investor demand, not because some separate asset “feeds” it. By contrast, in mortgage-backed and other structured deals, a floater tranche and an inverse-floater tranche are often carved from the same pool of collateral—typically fixed-rate loans or bonds whose gross coupon is (approximately) fixed as a share of outstanding principal.

What the collateral supplies. Think of the collateral as paying a total scheduled interest each period (for example a fixed pass-through coupon on a pool of mortgages, before prepayments and defaults complicate the picture). That single stream of cash interest is allocated across tranches according to deal rules. The structurer’s problem is to split that fixed (or mostly fixed) pie so that some investors receive floating coupons and others receive the remainder in a form that moves inversely with the chosen index.

The residual logic. A common pattern is:

- A floater tranche with face \(F\) earns a coupon such as \(\text{reference rate} + \text{margin}\) on \(F\).

- An inverse-floater tranche with face \(I\) earns whatever interest is left over from the collateral after the floater (and fees) are paid, expressed as a formula \(K - a \times \text{reference rate}\) on \(I\).

By construction, interest paid to the floater plus interest paid to the inverse floater (plus senior fees) adds up to the interest coming off the collateral (up to caps/floors and modelling simplifications). The two tranches are therefore not independent bets on unrelated assets; they are complementary claims on the same underlying cash flows. When the reference rate rises, the floater’s share of that pie rises and the inverse floater’s share must fall—hence the inverse coupon formula.

Who holds which piece. The floater tranche appeals to investors who want money-market–like duration and a known spread over the index. The inverse tranche concentrates interest-rate risk in investors who want higher potential income when rates fall and accept large price and income volatility when rates rise. The collateral’s credit/prepayment risk is typically shared according to the deal’s waterfall (sometimes one tranche is more subordinated than the other); the split of rate risk between floater and inverse is a separate design choice.

TipIntuition: One fixed coupon, two rate exposures

Picture a fixed-rate pool paying 6% on $100~million. If one tranche is structured to receive “SOFR + 0.5%” on $60~million, that tranche grabs more dollars whenever SOFR rises. Whatever interest remains for the other $40~million must fall—so that second tranche behaves like an inverse floater relative to SOFR. You have one source of interest; floating and inverse are just different rules for dividing the same collateral income.

NoteExample: Splitting collateral interest between floater and inverse

Simplified numbers: underlying collateral has $100~million principal and pays a fixed 6% annual interest, so $6~million per year before fees. Tranche F (floater): $60~million face, coupon SOFR + 0.50% paid on that $60~million. Tranche I (inverse): $40~million face; it receives all remaining interest on the pool after tranche F is paid (ignoring fees).

If SOFR is 5%, tranche F receives \((0.05 + 0.005) \times 60{,}000{,}000 = 3{,}300{,}000\) dollars per year. The residual for tranche I is \(6{,}000{,}000 - 3{,}300{,}000 = 2{,}700{,}000\), which is 6.75% on $40~million.

If SOFR rises to 7%, tranche F receives \((0.07 + 0.005) \times 60{,}000{,}000 = 4{,}500{,}000\). The residual for I is \(6{,}000{,}000 - 4{,}500{,}000 = 1{,}500{,}000\), which is 3.75% on $40~million. The floater’s coupon rose with SOFR; the inverse tranche’s coupon fell, even though the underlying collateral was still a fixed 6% pool—repackaging, not a second independent borrower promise.

Real CMOs add caps, floors, prepayment uncertainty, servicing, and credit enhancement; the economic point—that floater and inverse share the collateral’s interest—remains the same.

9 Price Quotes and Accrued Interest

9.1 Price Quotes

Bond prices are typically quoted as a percentage of par value. For example, a price quote of 98.50 means the bond is selling for 98.50% of its face value.

If the face value is $1,000, the price is

\[ 0.985 \times 1000 = 985. \]

Bond prices are quoted as clean prices, which do not include accrued interest.

9.2 Accrued Interest

When a bond is purchased between coupon payments, the buyer must pay the seller the interest that has accrued since the last coupon payment. This is called accrued interest.

The actual amount paid for a bond is called the dirty price:

\[ \text{Dirty Price} = \text{Clean Price} + \text{Accrued Interest}. \]

Accrued interest is calculated as

\[ \text{Accrued Interest} = \text{Coupon Payment} \times \frac{\text{Number of Days Since Last Coupon}}{\text{Number of Days in Coupon Period}}. \]

10 Computing the Yield or Internal Rate of Return on Any Investment

The yield of a bond is the discount rate that equates the present value of the bond’s expected cash flows to its market price. In other words, the yield is the internal rate of return (IRR) on the bond if the bond is held to maturity and all coupon payments are reinvested at the same rate.

Mathematically, the yield \(y\) is the rate that solves

\[ P = \sum_{t=1}^{n} \frac{CF_t}{(1+y)^t}. \]

This equation generally cannot be solved algebraically and must be solved using numerical methods or financial calculators.

10.1 Special Case: Investment with Only One Future Cash Flow

For a zero-coupon bond, there is only one future cash flow. The yield can therefore be calculated directly:

\[ P = \frac{F}{(1+y)^n} \]

Solving for \(y\):

\[ y = \left(\frac{F}{P}\right)^{1/n} - 1. \]

10.2 Annualizing Yields

If interest is compounded more than once per year, the annual yield must be adjusted. If the periodic rate is \(r/m\), then the effective annual rate is

\[ (1 + r/m)^m - 1. \]

This is called the effective annual yield.

11 Conventional Yield Measures

There are several different yield measures used in fixed income markets. Each yield measure answers a slightly different question.

11.1 Current Yield

The current yield measures the annual coupon income relative to the bond’s price:

\[ \text{Current Yield} = \frac{\text{Annual Coupon}}{\text{Bond Price}}. \]

Current yield ignores capital gains and reinvestment income, so it is an incomplete measure of return.

11.2 Yield to Maturity

Yield to maturity (YTM) is the internal rate of return assuming:

- The bond is held to maturity

- All coupon payments are reinvested at the YTM

- All payments are made as promised

YTM is the most commonly quoted yield measure.

11.3 Bond Calculators

Because the yield to maturity must be solved numerically, it is typically computed using financial calculators, spreadsheet software, or numerical algorithms.

NoteBond Price Calculator

Face Value Coupon Rate (%) Yield (%)

Years to Maturity Payments per Year

NoteYield to Maturity Calculator

Face Value Coupon Rate (%) Bond Price

Years to Maturity Payments per Year

11.4 Yield to Call

Many bonds give the issuer the right to redeem the bond before maturity at a specified call price. For such bonds, investors often compute the yield to call (YTC) instead of the yield to maturity.

The yield to call is the yield assuming:

- The bond is called at the first call date

- All coupon payments are received until the call date

- The bond is redeemed at the call price

- Coupons are reinvested at the yield to call

The yield to call is therefore the internal rate of return that equates the current price of the bond to the present value of the cash flows received until the call date.

If the bond is callable in \(n\) periods and the call price is \(F_{\text{call}}\), then the yield to call \(y_c\) is the rate that satisfies

\[ P = \sum_{t=1}^{n} \frac{C}{(1+y_c)^t} + \frac{F_{\text{call}}}{(1+y_c)^n}. \]

The yield to call is calculated in the same way as yield to maturity, except that:

- The maturity date is replaced by the call date

- The face value is replaced by the call price

Investors compute yield to call because if interest rates fall, the issuer may call the bond and refinance at a lower interest rate. In that case, the investor will earn the yield to call rather than the yield to maturity.

NoteWorked Example

Yield to Call

Suppose a bond has

- Price = $1,080

- Face value = $1,000

- Annual coupon rate = 8%

- Annual coupon payment = $80

- First call date = 4 years from now

- Call price = $1,040

The yield to call is the discount rate \(y_c\) that solves

\[ 1080 = \frac{80}{(1+y_c)} + \frac{80}{(1+y_c)^2} + \frac{80}{(1+y_c)^3} + \frac{1120}{(1+y_c)^4}. \]

Trying \(y_c = 6\%\) gives

\[ \frac{80}{1.06} + \frac{80}{1.06^2} + \frac{80}{1.06^3} + \frac{1120}{1.06^4} = 75.47 + 71.20 + 67.17 + 887.12 = 1100.96 \]

This is too high, so the yield must be higher.

Trying \(y_c = 6.5\%\) gives

\[ \frac{80}{1.065} + \frac{80}{1.065^2} + \frac{80}{1.065^3} + \frac{1120}{1.065^4} = 75.12 + 70.53 + 66.23 + 868.63 = 1080.51 \]

This is very close to the market price, so the yield to call is approximately

\[ y_c \approx 6.5\%. \]

Thus, if the bond is called in 4 years at $1,040, the investor’s yield to call is about 6.5%.

11.5 Yield to Sinker

Yield to sinker is the yield assuming the bond is retired through a sinking fund.

NoteWorked Example

Yield to Sinker

Suppose a company issues a $1,000 face value bond with the following features: - Annual coupon: 7% - Issue price: $980 - Sinking fund payments: $200 of principal will be retired at par at the end of each of years 3, 4, 5, 6, and 7. - Any remaining principal is paid at maturity (end of year 7).

You purchase one bond at issue and are selected for sinking fund calls, so your principal is repaid as follows:

| Year | Coupon Payment | Principal Repaid | Total Payment |

|---|---|---|---|

| 1 | $70 | $0 | $70 |

| 2 | $70 | $0 | $70 |

| 3 | $70 | $200 | $270 |

| 4 | $70 | $200 | $270 |

| 5 | $70 | $200 | $270 |

| 6 | $70 | $200 | $270 |

| 7 | $70 | $200 | $270 |

To find the yield to sinker (\(y_s\)), you solve for the discount rate that makes the purchase price equal to the present value of these projected cash flows:

\[ 980 = \sum_{t=1}^{7} \frac{\text{Total Payment}_t}{(1+y_s)^t}. \]

This requires trial and error or a financial calculator. Suppose, after calculation, you find \(y_s \approx 7.4\%\).

Key point:

The yield to sinker reflects the projected return if your bond is retired on the schedule dictated by sinking fund calls, which may be earlier than final maturity. It is generally compared to the YTM (if held to maturity) and yield to call (if callable) to assess your possible investment outcomes.

11.6 Yield to Put

Yield to put is the yield assuming the investor exercises the put option and sells the bond back to the issuer at the put price.

NoteWorked Example: Yield to Put

Yield to Put

Suppose you buy a $1,000 face value bond issued at par ($1,000) with the following features: - Coupon: 6% paid annually - Maturity: 10 years - Embedded put option: The bondholder may sell (put) the bond back to the issuer at par ($1,000) at the end of year 5

Assume current market yields rise, and you expect to exercise the put at the end of year 5. What is your yield to put if you exercise the put?

Projected cash flows if put is exercised:

| Year | Coupon Payment | Principal Repayment | Total Payment |

|---|---|---|---|

| 1 | $60 | $0 | $60 |

| 2 | $60 | $0 | $60 |

| 3 | $60 | $0 | $60 |

| 4 | $60 | $0 | $60 |

| 5 | $60 | $1,000 | $1,060 |

You paid $1,000 at issue. The yield to put (\(y_p\)) is the discount rate that equates the present value of the expected cash flows to the purchase price over 5 years:

\[ 1{,}000 = \frac{60}{(1+y_p)^1} + \frac{60}{(1+y_p)^2} + \frac{60}{(1+y_p)^3} + \frac{60}{(1+y_p)^4} + \frac{1{,}060}{(1+y_p)^5} \]

Solving this equation (trial and error, or a financial calculator), you find \(y_p \approx 6\%\).

Key point:

The yield to put reflects your expected return if you exercise the embedded put option at the first (or chosen) put date. It may be higher or lower than the yield to maturity, depending on the bond’s price, coupons, and market interest rates.

11.7 Yield to Worst

Yield to worst is the lowest yield among all possible yield measures (YTM, YTC, YTP, etc.). This is often used as a conservative measure of return.

11.8 Cash Flow Yield

Cash flow yield is the internal rate of return based on the expected cash flows, which may differ from the promised cash flows due to embedded options or prepayments.

NoteWorked Example: Cash Flow Yield

Cash Flow Yield

Suppose you are analyzing an amortizing asset-backed security (ABS) with the following expected cash flows due to scheduled principal repayments and prepayments. The bond is purchased for $5,000.

| Year | Expected Cash Flow |

|---|---|

| 1 | $1,200 |

| 2 | $1,400 |

| 3 | $1,100 |

| 4 | $800 |

| 5 | $700 |

The cash flow yield (\(y_{cf}\)) is the discount rate that equates the present value of these expected cash flows to the purchase price:

\[ 5{,}000 = \frac{1{,}200}{(1+y_{cf})^1} + \frac{1{,}400}{(1+y_{cf})^2} + \frac{1{,}100}{(1+y_{cf})^3} + \frac{800}{(1+y_{cf})^4} + \frac{700}{(1+y_{cf})^5} \]

Solving this equation (typically with a financial calculator or spreadsheet), you find \(y_{cf} \approx 6.2\%\).

Key point:

The cash flow yield reflects the average annual return to the investor, taking into account the timing and amount of the expected cash flows, including any prepayments or early principal repayments, not just the promised payments.

11.9 Yield (Internal Rate of Return) for a Portfolio

The yield for a bond portfolio is the internal rate of return that equates the total market value of the portfolio to the present value of the expected cash flows from all bonds in the portfolio.

In other words, the portfolio yield is the single discount rate that makes

\[ \text{Market Value of Portfolio} = \sum_{t=1}^{n} \frac{\text{Portfolio Cash Flow}_t}{(1+y)^t}. \]

This yield measure treats the entire portfolio as if it were a single bond with cash flows equal to the sum of the cash flows from all bonds in the portfolio.

The portfolio yield is useful because it provides a single summary measure of return for a portfolio containing many bonds with different coupons and maturities.

NoteWorked Example

Portfolio Yield

Suppose a portfolio consists of two bonds:

| Bond | Market Value | Cash Flow in 1 Year | Cash Flow in 2 Years |

|---|---|---|---|

| A | 950 | 60 | 1,060 |

| B | 980 | 50 | 1,050 |

Total market value of the portfolio:

\[ 950 + 980 = 1,930 \]

Total portfolio cash flows:

| Year | Cash Flow |

|---|---|

| 1 | 60 + 50 = 110 |

| 2 | 1060 + 1050 = 2110 |

The portfolio yield \(y\) solves

\[ 1930 = \frac{110}{(1+y)} + \frac{2110}{(1+y)^2}. \]

Trying \(y = 6\%\):

\[ \frac{110}{1.06} + \frac{2110}{1.06^2} = 103.77 + 1877.34 = 1981.11 \]

Too high → yield must be higher.

Trying \(y = 8\%\):

\[ \frac{110}{1.08} + \frac{2110}{1.08^2} = 101.85 + 1808.45 = 1910.30 \]

Too low → yield must be between 6% and 8%.

Trying \(y = 7\%\):

\[ \frac{110}{1.07} + \frac{2110}{1.07^2} = 102.80 + 1843.68 = 1946.48 \]

Close to the market value, so the portfolio yield is approximately

\[ y \approx 7\%. \]

Thus, the internal rate of return for the portfolio is approximately 7%.

11.10 Yield Spread Measures for Floating-Rate Securities

Floating-rate securities are quoted using spread measures such as:

- Discount margin

- Quoted margin

- Spread over reference rate

These spreads measure the compensation investors receive above the reference rate.

NoteWorked Example: Discount Margin for a Floating-Rate Note

Discount Margin Example:

Suppose you are analyzing a floating-rate note (FRN) with the following features:

- Face value: $1,000

- Coupon rate: 3-month SOFR + 1.20% (set at each reset date)

- Coupon paid quarterly

- Current 3-month SOFR: 4.60%

- Quoted margin: 1.20%

- Price: $1,002.00 (per $1,000 face value)

- 90 days to next reset

Step 1: Calculate the next coupon payment

\[ \text{Next coupon rate} = 4.60\% + 1.20\% = 5.80\% \]

\[ \text{Quarterly coupon payment} = 1{,}000 \times \frac{5.80\%}{4} = 14.50 \]

Step 2: Estimate the Discount Margin

The discount margin (\(DM\)) is the spread that equates the present value of the expected cash flows (assuming the reference rate remains unchanged) to the observed price.

For a floating-rate note, cash flows are based on the quoted margin, while discounting is done using the discount margin:

\[ \text{Price} = \sum_{t=1}^{n} \frac{\left(\frac{\text{Reference Rate} + \text{Quoted Margin}}{m}\right) \times 1{,}000} {\left(1 + \frac{\text{Reference Rate} + DM}{m}\right)^t} + \frac{1{,}000} {\left(1 + \frac{\text{Reference Rate} + DM}{m}\right)^n} \]

where: - \(m = 4\) (quarterly payments)

- \(n\) = number of remaining periods

- Reference Rate = 4.60%

- Quoted Margin = 1.20%

Since the FRN is trading slightly above par (\(1{,}002 > 1{,}000\)), the discount margin must be slightly less than the quoted margin.

The exact value of \(DM\) depends on the bond’s maturity and is obtained numerically using a financial calculator or spreadsheet.

Key point:

The discount margin is a more appropriate yield measure for floating-rate notes than yield to maturity because it captures the investor’s expected return relative to the reference rate, given the bond’s price and floating cash flow structure.

12 Potential Sources of a Bond’s Dollar Return

The total dollar return from a bond comes from three sources:

- Coupon income

- Interest earned from reinvesting coupons (interest-on-interest)

- Capital gain or loss if the bond price changes

NoteSummary: Yield Measures and Sources of Bond Return

When assessing a bond’s potential yield, it is crucial to recognize that total return can originate from three sources: coupon interest, reinvestment of coupons (interest-on-interest), and capital gain or loss. Different yield measures consider these sources differently:

- Current Yield: Considers only coupon interest; ignores reinvestment income and capital gains or losses.

- Yield to Maturity (YTM): Reflects all three sources, but only if:

- The bond is held to maturity, and

- Coupon payments are reinvested at the YTM rate. Otherwise, the realized yield may differ from the stated YTM.

- Yield to Call (YTC): Also incorporates all three sources, assuming:

- The bond is called on the specified call date,

- Coupons are reinvested at the YTC rate. This measure faces the same reinvestment assumption risk as YTM.

- Cash Flow Yield: Like YTM, but also assumes:

- Principal repayments are reinvested at the cash flow yield, and

- Projected prepayment patterns actually occur.

Key Point: All yield measures that include capital gains/losses and interest-on-interest rely on significant reinvestment and holding period assumptions. When these assumptions are not met, the actual realized yield may be higher or lower than stated.

12.1 Determining the Interest-on-Interest Dollar Return

When a bond pays periodic coupons, investors typically reinvest those coupon payments until the end of the investment horizon. The interest earned on reinvested coupons is called interest-on-interest. This component of return can be significant, especially for long-term bonds, and it is an important part of the total return of a bond investment.

If a coupon payment \(C\) is received and reinvested for \(k\) periods at a reinvestment rate \(r\), the future value of that coupon at the end of the horizon is

\[ C(1+r)^k. \]

The interest-on-interest is the future value of the reinvested coupon minus the coupon itself:

\[ \text{Interest-on-Interest} = C(1+r)^k - C. \]

For a bond that pays coupons over multiple periods, the total interest-on-interest is the sum of the interest earned on each reinvested coupon:

\[ \text{Total Interest-on-Interest} = \sum_{t=1}^{n} \left[ C(1+r)^{n-t} - C \right]. \]

This formula shows that earlier coupon payments earn interest for a longer period of time and therefore contribute more to the total return than later coupon payments.

NoteWorked Example

Interest-on-Interest Return

Suppose an investor buys a bond that pays $80 per year in coupons for 3 years. Each coupon is reinvested at an interest rate of 5% until the end of year 3.

Future value of each coupon at the end of year 3:

- Coupon at end of year 1 grows for 2 years:

\[ 80(1.05)^2 = 88.20 \]

- Coupon at end of year 2 grows for 1 year:

\[ 80(1.05) = 84.00 \]

- Coupon at end of year 3 is received at the horizon:

\[ 80 \]

Total future value of coupons:

\[ 88.20 + 84.00 + 80 = 252.20 \]

Total coupons received:

\[ 80 + 80 + 80 = 240 \]

Interest-on-interest:

\[ 252.20 - 240 = 12.20 \]

Thus, $12.20 of the investor’s return comes from interest earned on reinvested coupons.

12.2 Yield to Maturity and Reinvestment Risk

Yield to maturity assumes that coupons are reinvested at the YTM. If reinvestment rates are lower than the YTM, the investor’s actual return will be lower. This is called reinvestment risk.

The potential total dollar return assumes all coupons are reinvested at the yield to maturity (YTM).

Worked Example

NoteWorked Example: Breaking Down the Total Dollar Return

Suppose an investor buys a 15-year bond for $769.40. The bond pays a 10% annual coupon, distributed as $50 every six months (i.e., semiannual coupons). The bond’s face value is $1,000 and its yield to maturity is 10% (so, 5% per half-year). We examine the components of the total dollar return if the bond is held to maturity and coupons are reinvested at the YTM.

Total Coupon Interest:

Over 15 years, there are \(15 \times 2 = 30\) semiannual periods.

\(50 \times 30 = 1,500\) in coupon payments.Interest-on-Interest (Reinvestment Effect):

Each coupon is reinvested at 5% per period. The future value of coupons is: \[ FV_{\text{coupons}} = 50 \times \frac{(1.05)^{30} - 1}{0.05} \approx 3,321.90 \] The incremental value due to reinvestment is: \[ 3,321.90 - 1,500 = 1,821.90 \]Capital Gain:

The bond is purchased at $769.40 and redeemed at \(1,000:\)$ 1,000 - 769.40 = 230.60 $$

Total Dollar Return: \[ 1,500 + 1,821.90 + 230.60 = 3,552.50 \]

Consistency check (future value of initial investment): \[ 769.40 \times (1.05)^{30} \approx 3,325.30 \]

Important note:

The small discrepancy between the two totals arises from rounding. Conceptually, the total future value equals the reinvested coupons plus the principal repayment.

Key point:

To realize the yield to maturity, an investor must reinvest all coupon payments at the YTM. If reinvestment rates are lower, the realized return will fall short of the YTM—this is reinvestment risk.

Reinvestment Risk and Bond Characteristics

Two characteristics influence how much of a bond’s total return depends on reinvestment:

- Maturity: Longer-maturity bonds are more sensitive to reinvestment risk. The longer the bond’s life, the more the total return depends on interest earned from reinvested coupons.

- Coupon Rate: The higher the coupon rate, the greater the proportion of total return that depends on reinvestment. Premium bonds (high-coupon) are more dependent on reinvestment than par or discount bonds.

Zero-coupon bonds have no reinvestment risk: all the return comes from the difference between purchase price and face value, with no intermediate coupons to reinvest. The yield actually realized for a zero-coupon bond held to maturity always equals its YTM at purchase.

Amortizing Securities and Reinvestment Risk

For amortizing securities, reinvestment risk is typically greater than for non-amortizing securities (such as conventional bullet bonds). With a bullet bond, the investor reinvests periodic coupon payments until maturity, when principal is returned in one lump sum. With an amortizing security, scheduled cash flows include both coupon interest and principal repayments, so the investor must reinvest principal as well as coupons throughout the life of the investment.

The reinvestment burden is often heavier still for the major types of amortizing securities covered later in this course—mortgage-backed securities (MBS) and asset-backed securities (ABS). Their cash flows are usually monthly, whereas coupons on non-amortizing bonds are typically semiannual. The investor must reinvest coupon income and returned principal more frequently, which increases reinvestment risk.

A further source of reinvestment risk on many amortizing structures is prepayment. Borrowers are often allowed to accelerate scheduled principal repayment. In practice, prepayment tends to rise when interest rates fall, because refinancing becomes attractive. If a borrower prepays when rates are lower, the investor receives principal sooner and must reinvest those funds at lower reinvestment rates—reinforcing reinvestment risk at exactly the time reinvestment is least attractive.

13 Total Return

In the preceding sections, we explained that the yield to maturity is a promised yield. At the time of purchase, an investor is promised the yield to maturity if both of the following conditions are satisfied:

- The bond is held to maturity.

- All coupon payments are reinvested at the yield to maturity.

In reality, these assumptions are often unrealistic. Investors may sell the bond before maturity, and coupon payments may be reinvested at interest rates different from the yield to maturity. Therefore, the yield to maturity may not represent the investor’s actual return.

To address this issue, investors use a measure called total return, which incorporates:

- The investor’s investment horizon

- The reinvestment rate for coupon payments

- The expected yield when the bond is sold at the end of the investment horizon

The total return is therefore a more realistic measure of the return on a bond investment.

13.1 Computing the Total Return for a Bond

The idea underlying total return is simple. We first compute the total future dollars that will be available at the end of the investment horizon. Then we compute the interest rate that makes the initial investment grow to this future value.

The steps are as follows:

Step 1: Compute the total coupon payments plus interest-on-interest based on the assumed reinvestment rate.

Step 2: Determine the projected sale price at the end of the investment horizon. This depends on the expected yield at that time.

Step 3: Add the reinvested coupons and the projected sale price. This gives the total future dollars.

Step 4: Compute the rate of return that makes the purchase price grow to the total future dollars.

If the investment horizon is \(h\) semiannual periods, the semiannual total return \(r\) is found from

\[ \left(\frac{\text{Total Future Dollars}}{\text{Purchase Price}}\right)^{1/h} - 1. \]

The annual total return is approximately

\[ \text{Total Return} = 2r \]

because interest is compounded semiannually.

NoteWorked Example 1: Total Return with Constant Reinvestment Rate

Suppose an investor with a 3-year investment horizon is considering purchasing a 20-year 8% coupon bond for $828.40. The yield to maturity is 10%. The investor expects:

- Reinvestment rate = 6% annually (3% per six months)

- Yield at end of horizon = 7%

- Coupons = $40 every six months

- Investment horizon = 6 semiannual periods

Step 1: Reinvest Coupons

The total coupon interest plus interest-on-interest is

\[ 40 \left( \frac{(1.03)^6 - 1}{0.03} \right) = 40(6.4684) = 258.74 \]

Step 2: Projected Sale Price

At the end of 3 years, the bond will have 17 years remaining to maturity (34 periods). The projected sale price is the present value of remaining cash flows discounted at 7% annual yield (3.5% per period):

Projected sale price = $1,098.51

Step 3: Total Future Dollars

\[ \text{Total Future Dollars} = 258.74 + 1,098.51 = 1,357.25 \]

Step 4: Compute Total Return

\[ \left(\frac{1357.25}{828.40}\right)^{1/6} - 1 = (1.6384)^{0.1667} - 1 = 0.0858 \]

Semiannual return = 8.58%

Annual total return:

\[ 2 \times 8.58\% = 17.16\% \]

Thus, the investor’s total return is 17.16%.

NoteWorked Example 2: Total Return with Multiple Reinvestment Rates

Suppose an investor has a 6-year investment horizon and purchases a 13-year 9% bond selling at par. The investor expects:

- First four coupon payments reinvested at 8% annually (4% per period)

- Remaining eight coupon payments reinvested at 10% annually (5% per period)

- Yield at end of horizon = 10.6%

Coupons are $45 every six months for 12 periods.

Step 1: Reinvest First Four Coupons

Future value at end of year 2:

\[ 45 \left( \frac{(1.04)^4 - 1}{0.04} \right) = 191.09 \]

Reinvest this amount for 8 more periods at 5%:

\[ 191.09(1.05)^8 = 282.32 \]

Step 2: Reinvest Remaining Eight Coupons

\[ 45 \left( \frac{(1.05)^8 - 1}{0.05} \right) = 429.71 \]

Total reinvested coupons:

\[ 282.32 + 429.71 = 712.03 \]

Step 3: Projected Sale Price

Discount remaining cash flows at 10.6% yield:

Projected sale price = $922.31

Step 4: Total Future Dollars

\[ 712.03 + 922.31 = 1,634.34 \]

Step 5: Total Return

\[ \left(\frac{1634.34}{1000}\right)^{1/12} - 1 = 0.0418 \]

Semiannual return = 4.18%

Annual total return:

\[ 2 \times 4.18\% = 8.36\% \]

Thus, the investor’s total return is 8.36%.

13.2 Key Insight

Total return depends on three key factors:

- Reinvestment rate

- Yield at the end of the investment horizon

- Investment horizon

Therefore, the total return measure allows investors to compare bonds with different maturities and coupon rates based on their own expectations about future interest rates and reinvestment opportunities.

14 Applications of Total Return (Horizon Analysis)

Horizon analysis is used by portfolio managers to estimate the return of a bond over a specific investment horizon.

It allows investors to analyze how returns change if:

- Interest rates change

- Reinvestment rates change

- The bond is sold before maturity

This approach is widely used in fixed income portfolio management.

NoteExample: Horizon Analysis in Practice

Scenario:

Suppose you purchase a 3-year bond with a face value of $1,000 and a 6% annual coupon, paid annually. You plan to sell the bond after 2 years, when you expect the yield to have changed.

- Bond characteristics:

- Coupon rate: 6%

- Face value: $1,000

- Annual coupon: $60

- Time to maturity at purchase: 3 years

- Purchase YTM: 6%

- Expected YTM at sale (after 2 years): 5%

- Investment horizon: 2 years

- Coupon rate: 6%

Since the coupon rate equals the YTM at purchase, the bond is initially priced at par ($1,000).

Step 1: Cash Flows During Holding Period

You receive two coupon payments: - Year 1: $60

- Year 2: $60

Step 2: Sale Price at End of Year 2

After 2 years, the bond has 1 year remaining. Its price reflects the new YTM of 5%:

\[ P_{2} = \frac{60}{1.05} + \frac{1,000}{1.05} = 57.14 + 952.38 = 1,009.52 \]

Step 3: Reinvestment of Coupons

Assume coupons are reinvested at 5% (the expected rate at the horizon):

- First coupon grows for 1 year: \[ 60 \times 1.05 = 63 \]

- Second coupon is received at the end of Year 2: \[ 60 \]

Step 4: Total Value at End of Horizon (2 Years)

- Sale proceeds: $1,009.52

- Value of reinvested coupons: $63 + 60 = 123

\[ \text{Total value} = 1,009.52 + 123 = 1,132.52 \]

Step 5: Horizon Return

Total 2-year return: \[ \frac{1,132.52 - 1,000}{1,000} = 13.25\% \]

Annualized (compound) return: \[ (1.13252)^{1/2} - 1 \approx 6.42\% \text{ per year} \]

Key Insight:

The realized (horizon) return depends on: - coupon income

- reinvestment rate of coupons

- the bond’s sale price (determined by yields at the horizon)

A decline in yields (from 6% to 5%) generates a capital gain, which raises the realized return above the initial YTM.

15 Calculating Yield Changes

When interest rates or yields change between two time periods, there are two common ways to measure the change:

- Absolute yield change

- Relative (percentage) yield change

These two measures are used in fixed income markets because yields are often reported in basis points and percentage changes.

15.1 Absolute Yield Change

The absolute yield change (also called the absolute rate change) is measured in basis points and is simply the absolute difference between two yields.

\[ \text{Absolute yield change (in basis points)} = | \text{Initial yield} - \text{New yield} | \times 100 \]

Recall:

\[ 1\% = 100 \text{ basis points} \]

NoteWorked Example

Suppose yields over three months are:

| Month | Yield |

|---|---|

| Month 1 | 4.45% |

| Month 2 | 5.11% |

| Month 3 | 4.82% |

Absolute yield change from Month 1 to Month 2:

\[ |4.45\% - 5.11\%| \times 100 = 0.66\% \times 100 = 66 \text{ basis points} \]

Absolute yield change from Month 2 to Month 3:

\[ |5.11\% - 4.82\%| \times 100 = 0.29\% \times 100 = 29 \text{ basis points} \]

Absolute changes are the most commonly used measure in bond markets because traders and portfolio managers typically discuss yield changes in basis points.

15.2 Relative (Percentage) Yield Change

The relative yield change measures the percentage change in yield and is computed using the natural logarithm:

\[ \text{Relative yield change} = 100 \times \ln \left(\frac{\text{New yield}}{\text{Initial yield}}\right) \]

This measure is often used in financial modeling because log changes are additive over time and are commonly used in statistical analysis and interest rate modeling.

NoteWorked Example

Using the same yields:

| Month | Yield |

|---|---|

| Month 1 | 4.45% |

| Month 2 | 5.11% |

| Month 3 | 4.82% |

Relative yield change from Month 1 to Month 2:

\[ 100 \times \ln\left(\frac{5.11}{4.45}\right) = 100 \times \ln(1.1483) = 100 \times 0.1383 = 13.83\% \]

Relative yield change from Month 2 to Month 3:

\[ 100 \times \ln\left(\frac{4.82}{5.11}\right) = 100 \times \ln(0.9433) = 100 \times (-0.0584) = -5.84\% \]

15.3 When to Use Each Measure

| Measure | Used For |

|---|---|

| Absolute change (basis points) | Bond markets, trading, duration/convexity |

| Relative change (log change) | Interest rate modeling, statistics, econometrics |

In practice, bond traders typically think in basis points, while researchers and risk modelers often use relative (log) yield changes.

Key Points

The foundation of bond valuation is the time value of money: the value of any fixed income security is the present value of its expected future cash flows.

Future value formulas show how a single payment or a sequence of payments grows over time through compounding, while present value formulas show how future cash flows are discounted back to the present.

A bond can be viewed as the sum of two components:

- the present value of its coupon payments

- the present value of its principal repayment at maturity

- the present value of its coupon payments

A zero-coupon bond is the simplest bond pricing case because it has only one cash flow at maturity.

Bond prices and yields move in opposite directions. When required yields rise, bond prices fall; when required yields fall, bond prices rise.

The price–yield relationship is convex, not linear. This means that price gains from falling yields are larger than price losses from equally sized yield increases.

The relationship between a bond’s coupon rate and its required yield determines whether it sells at par, at a premium, or at a discount.

If interest rates remain unchanged, a bond’s price moves toward its face value as maturity approaches. This is the pull-to-par effect.

Bond prices can change because of changes in market interest rates, credit risk, liquidity, inflation expectations, tax treatment, and general economic conditions.

In practice, bond pricing is more complicated when the next coupon date is less than a full period away, when cash flows are uncertain, when the correct discount rate is difficult to determine, or when different cash flows should be discounted at different rates.

Floating-rate securities and inverse floaters require special treatment because their coupon payments depend on future interest rates.

Bonds are usually quoted using clean prices, while the actual transaction price is the dirty price, which includes accrued interest.

The yield on any investment is the internal rate of return that equates the price of the investment to the present value of its cash flows.

When there is only one future cash flow, yield can be computed directly. When there are multiple cash flows, yield usually must be solved numerically.

Conventional yield measures include current yield, yield to maturity, yield to call, yield to sinker, yield to put, yield to worst, cash flow yield, and the yield for a portfolio.

Current yield considers only coupon income and ignores both capital gains or losses and reinvestment income.

Yield to maturity assumes that the bond is held to maturity and that all coupon payments are reinvested at the yield to maturity. For this reason, it is a promised yield, not necessarily the realized yield.

Yield to call, yield to put, and yield to sinker are computed in the same general way as yield to maturity, but they assume that the bond is redeemed on the relevant call, put, or sinking-fund date.

Yield to worst is the lowest yield among the relevant yield measures and is commonly used as a conservative measure of return.

The yield for a portfolio is not simply an average of the yields of the individual bonds. It is the internal rate of return that equates the market value of the portfolio to the present value of the portfolio cash flows.

For floating-rate securities, investors often use spread measures such as the discount margin rather than conventional yield measures.

A bond’s dollar return comes from three sources:

- coupon income

- reinvestment income

- capital gain or loss

- coupon income

The interest-on-interest component can represent a large share of total return, especially for long-term coupon bonds.

Because yield to maturity assumes reinvestment at the same yield, investors face reinvestment risk when actual reinvestment rates differ from the assumed rate.

Reinvestment risk is especially important for high-coupon bonds, long-maturity bonds, and amortizing securities.

Total return is a more realistic measure of performance than conventional yield measures because it explicitly incorporates the investor’s holding period, reinvestment assumptions, and expected sale price.

To compute total return, one must determine:

- the future value of reinvested coupon payments

- the projected sale price at the end of the investment horizon

- the rate of return that equates the initial purchase price to total future dollars

- the future value of reinvested coupon payments

Horizon analysis applies the total return framework to a specific investment horizon and is widely used in fixed income portfolio management.

Yield changes can be measured in two common ways:

- absolute yield changes, usually expressed in basis points

- relative yield changes, often computed using logarithms

- absolute yield changes, usually expressed in basis points

In practice, traders usually focus on basis-point changes, while relative yield changes are often more useful in modeling and statistical analysis.

16 Readings

Fabozzi – Bond Markets, Analysis, and Strategies:

Chapter 2: Pricing of Bonds

Chapter 3: Measuring Yield